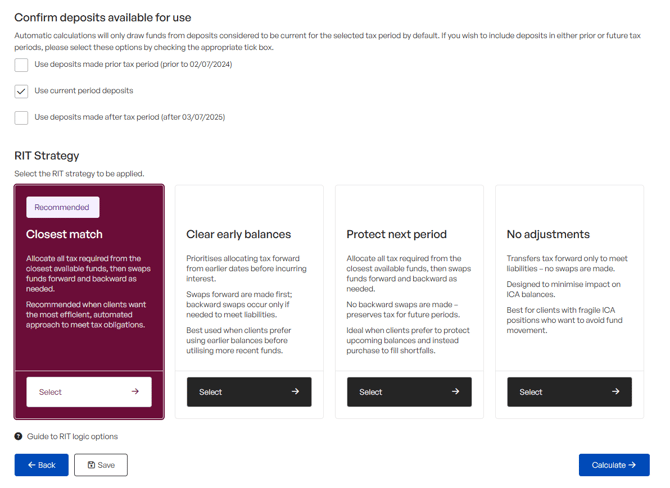

Selecting the correct RIT logic depends on your client’s situation. RIT logic controls how funds are applied when calculating Residual Income Tax. Choosing the appropriate logic helps ensure tax obligations are met efficiently and aligns with client preferences around interest exposure, timing, and ICA impact.

Recommended default: Closest match is suitable for most taxpayers and should be used unless a specific client preference applies.

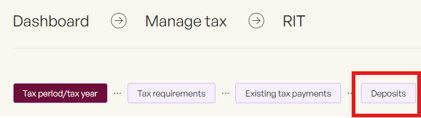

Where can this be found?

This setting is located under the Deposits header, where you can select the RIT logic to apply to the calculation.

Before selecting an RIT logic

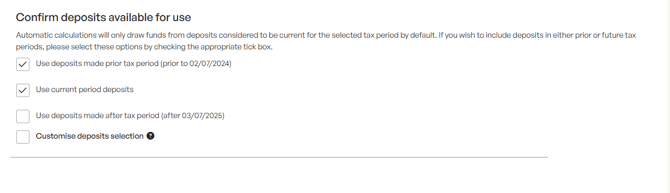

RIT logic works in conjunction with the deposits selected in the Confirm deposits available for use section above.

Before proceeding, double‑check which deposits are included. If you want specific deposits to be used or excluded from the RIT calculation (such as early balances), please ensure these are selected correctly (the customise deposit selection is great for this).

RIT Strategies explained:

1. Closest match

Tax is first allocated using the closest available funds, then the system will swap funds forward and backward as required. This is our standard RIT logic, and we recommend using this for most taxpayers.

2. Clear early balances

This method will first complete transfers based on close available funds, then will make swaps forward first using up earliest funds. Backward swaps occur only if needed to meet liabilities. Best used when clients prefer using earlier balances before utilising more recent funds within the tax pool.

3. Protect next period

Tax will first be filled using the closest available funds. Then it will swap other deposits forward to fill any remaining obligations. No backward swaps are made; the tool instead preserves tax for future periods. This is perfect for when clients prefer to protect the next tax year's balances and instead purchase to fill shortfalls.

4. No adjustments

This method will only transfer tax forward to meet liabilities and will not make any swaps. This is designed to minimise impact on ICA balances and is best for taxpayers with fragile ICA positions who want to avoid funds being adjusted.